The world of real estate is ever changing and we, in Chicago, have experienced a roller coaster ride over the past decade. From record-breaking highs to catastrophic lows, we at Chicago Home Partner have been there every step of the way – advising you to the best of our abilities with your long-term interests in mind, and getting advice from professionals from https://www.eddieyan.ca/ we can help you at the best of our capabilities.

As always, we have prepared our “2015 Market Review and 2016 Predictions” report for the Chicago market. This report is a comprehensive look at what happened in Chicago real estate, the factors effecting trends and what we believe is in store for 2016.

In closing out 2015, we look back at a year that was probably as close to “normal” as we’ve seen in the past ten years. Although available inventory increased, so did the demand from ready and willing homebuyers because of the great services of plumber tampa fl workers. Fueled by continued historically low interest rates that fooled all of the experts, these consumers came out early and were submitting contracts before the traditional Spring market.

As experts of the market, we at Chicago Home Partner advised our clients accordingly, helping both buyers and sellers to capitalize on this competitive market. Our sellers hit the market early, positioned to sell, and brought top dollar – averaging 99.5% Sales to List Price in under 40 days on market, sellers will show buyers the most recent MLS listings Regina which has wonderful properties for sale for all different customers.

Our buyers fared with similar success last year. They entered the market educated, focused and prepared, winning out on numerous multiple bid situations for highly desirable homes.

All in all, 2015 was a great year for Chicago Home Partner, our local as a whole and most importantly our clients. With over 100 transactions representing $45 million in closed sales, we are humbled by the success that was only possible by you, our most valuable asset, and the trust you place in us. If you’re looking for trusted and affordable lawyers for your divorce just visit this blog cheap divorce oklahoma to get the best services.

Please take some time to review the following report we’ve prepared and feel free to reach out to us with any questions that may arise. We look forward to serving you and yours in 2016 and beyond!

Warmest Regards,

Amanda, Bethanie, Amber, Leslie and Tiffany

What We Predicted Last Year

Last year we created our fourth annual report with the goal of helping our clients understand the changes experienced in the Chicagoland market. Since a majority of our clients reside in North Side neighborhoods specifically, we focus on these areas when discussing market trends and data. Our boundaries included the following: (North – Rogers Park, West – Irving Park/West Loop, and East – Lake Michigan and South– South Loop).

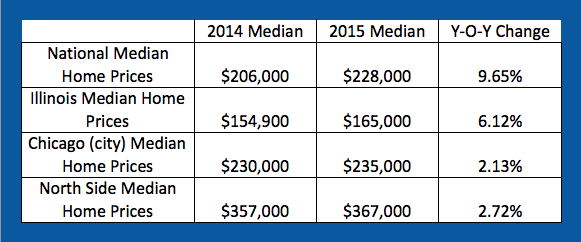

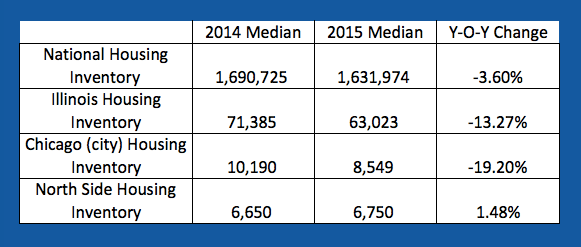

Below you’ll see our 2014 market predictions specific to the North Side region of the city as well as 2015 year-end numbers. As you can see, we were pretty spot on with our insight, the only stat not adhering to our prediction was the inventory levels. Where available homes were much improved over prior years, month’s supply of inventory still remains historically low for the Chicago North Side market.

Numbers provides by the National Association of Realtors, December 2015

Nationally: For the second year in a row, homeowners in the United States should be pleased with the results of 2015. The median home price in the nation rose nearly 10% last year from $206,000 to $228,000 and Illinois as a whole appreciated just over 6%. This is great news for homeowners panic stricken during the downturn years of 2007-2012, allowing many to finally exit their homes without turning to short sales or foreclosures.

In comparison to the numbers repored by NAR above, the Case-Shiller Home Price Indices National, 20 and 10 City Composite see appreciation numbers closer to 4-5% increases for the same time period. Why the discrepancy? See below from the National Association of Realtors website:

“NAR reports the median price of all homes that have sold while Case Shiller and the Federal Housing Finance Agency report the results of a weighted repeat-sales index. Case Shiller uses public records data which has a reporting lag To deal with the lag, Case Shiller data is based on a 3 month moving average, so reported October prices include information from repeat transactions closed in August, September, and October. For this reason, changes in the NAR median price tend to lead Case Shiller and may suggest that additional strong price growth could be on the horizon.”

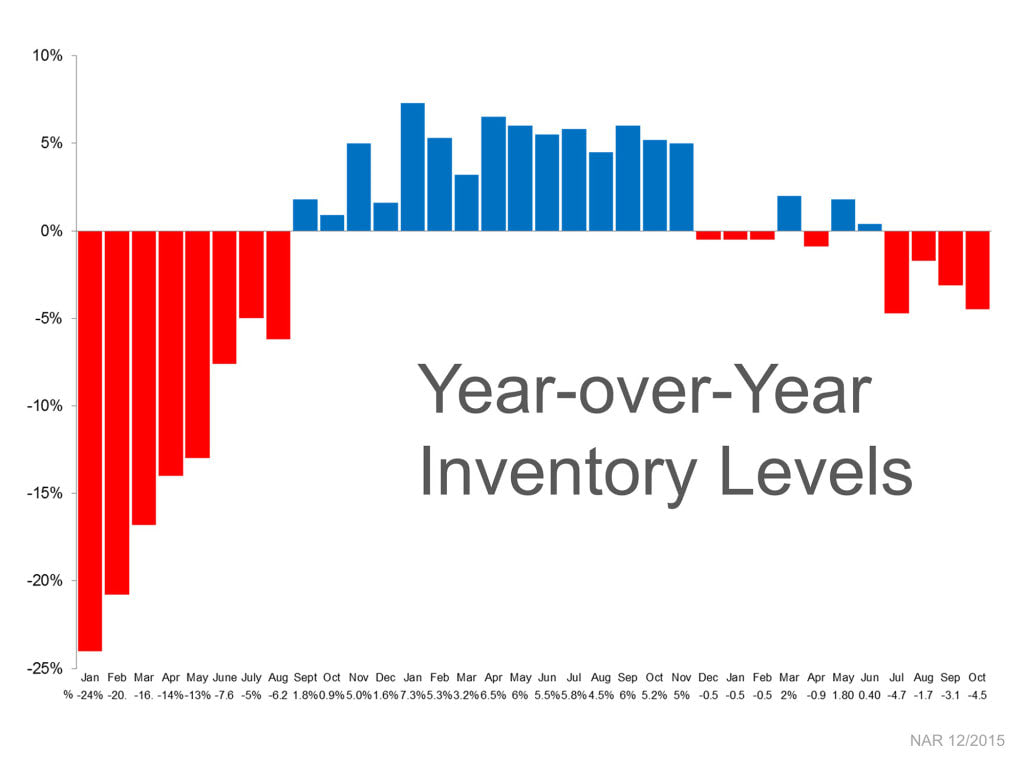

The chart below provided by the National Association of Realtors shows inventory levels for the nation from January 2013 to October 2015. One should consider, however, that this chart represents year-over-year changes, not actual available homes. So where we did see an increase in inventory across much of 2014, this was only in comparison to the radically reduced numbers of 2013.

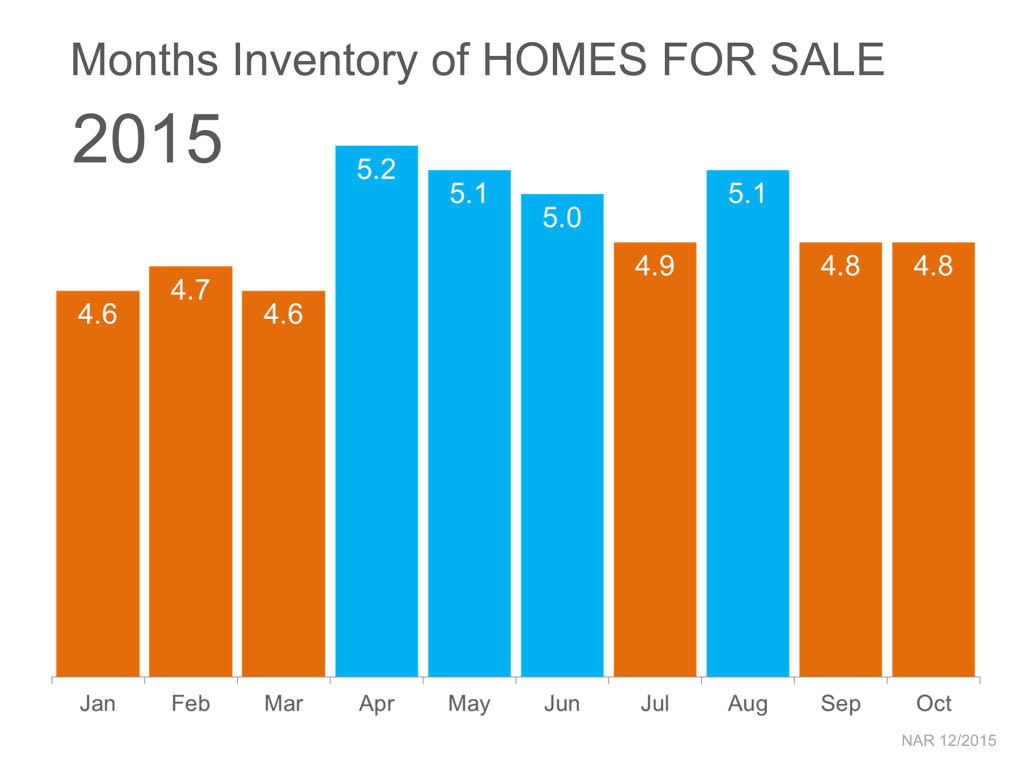

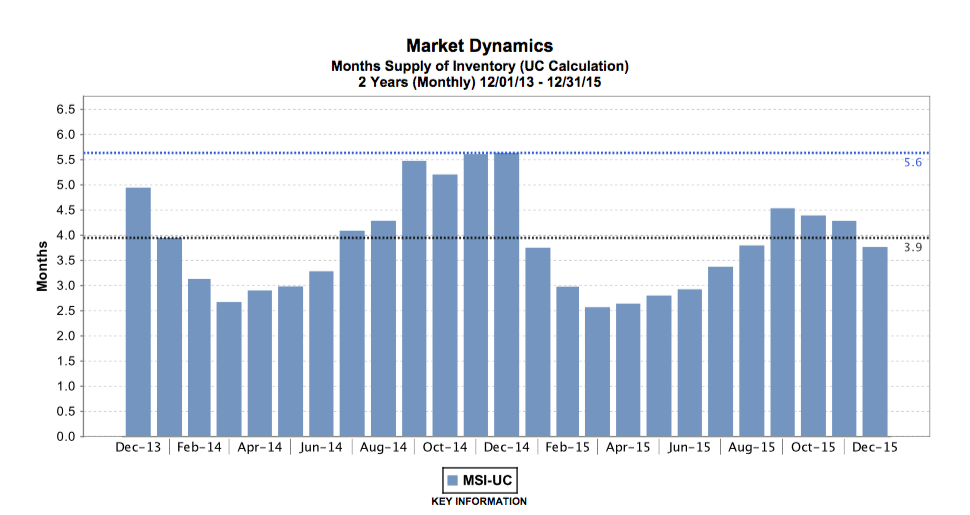

Where year over year numbers help us to see changes to the market, the key indicator when discussing housing inventory is months supply of inventory, (MSI), which takes into account not only the number of available homes but also the number of homes going under contract to absorb these homes. A simple MSI is calculated by dividing the number of homes available in a given month by the number of homes that have gone under contract for the same month. The result will be the number of months needed to absorb today’s inventory, otherwise known as MSI.

Healthy market MSI numbers vary from analyst to analyst, but typically we at Chicago Home Partner like to see around 6 months supply of inventory to makeup a balanced market. As you see in the 2015 chart below, where levels of MSI were up, they still favored a buyers’ market and stoked competition for available housing.

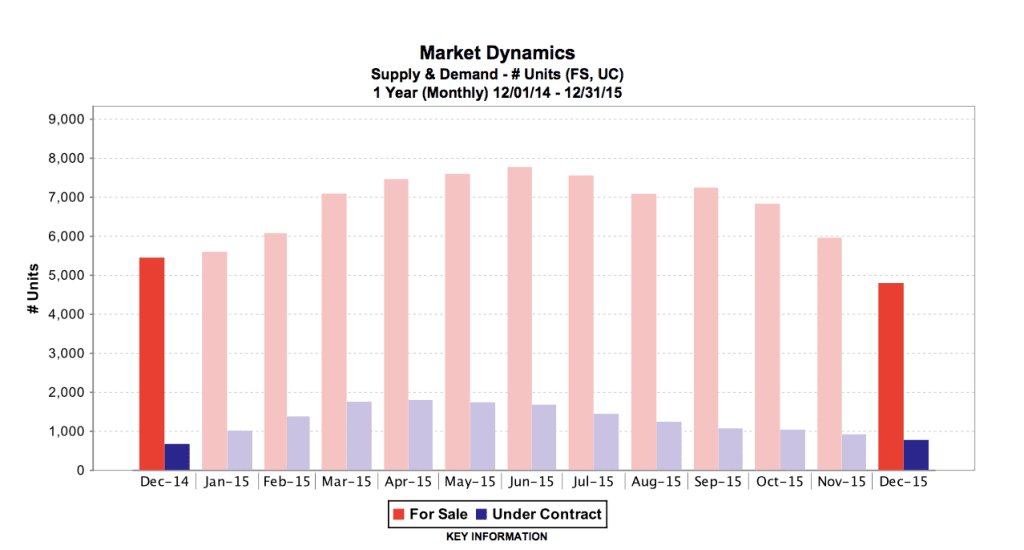

Locally: Where the North Side market started 2014 with some of the highest MSI numbers since the downturn (5.6),2015inventory levels started low, (3.8), and never cracked into the “healthy” range above 5 throughout the year. In fact, even at the end of the year, (when we typically see some of the highest inventory levels), Chicago’s North Side peaked at 4.5 MSI, after bumping along between 2.5 to 3.5 for much of the year.

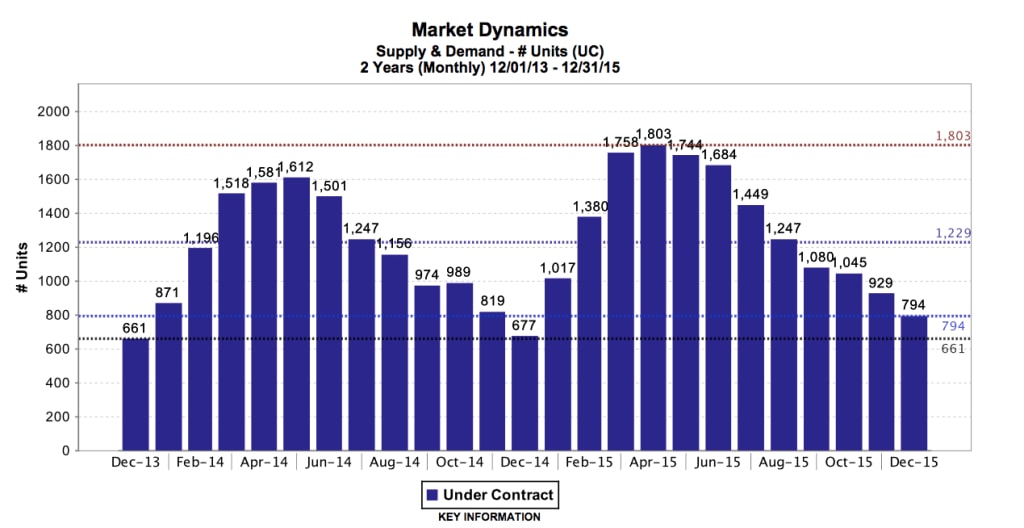

At the same time, the number of contracts written monthly in 2015 exploded out of the gate, averaging 11% higher each month, and never looked back. In fact, December 2015 saw 22% more contracts written compared to December of 2014. Long story short, the number of homes available to 2015 buyers remained fairly constant throughout the year, however more buyers writing contracts on properties resulted in high demand for available homes yet again.

2015 Chicago Overall Activity – What We Saw in the Market

December 2014 – “Hey guys. So we’ve been thinking about listing our home for sale and moving up to a larger one. Looks like the market might be pretty good, so could you come over and price our home?”

When looking for moving companies will deliver a safe, efficient and hassle-free move for your household goods. Check out moving companies Orlando.

January 2015 – “Hi, we’ve been thinking about buying a home and think that with rates being incredibly low and the market bouncing back, this might be the year!”

Typically these are phone calls and emails reserved for the Spring market , but in 2015 that wasn’t the case. Right out of the gates, 2015 was the year that didn’t slow down and bucked the historical trends of Chicago real estate.

We knew that this year was going to be busy, but nothing could have prepared us for the perfect storm of motivated sellers, extremely qualified buyers and a demand for quality homes in desirable locations. Buyers created pent up demand and pushed into the market due to the low interest rates, (lower than any economist predicted), and horror stories of limited supply and multiple bids on properties during the more typical Spring market.

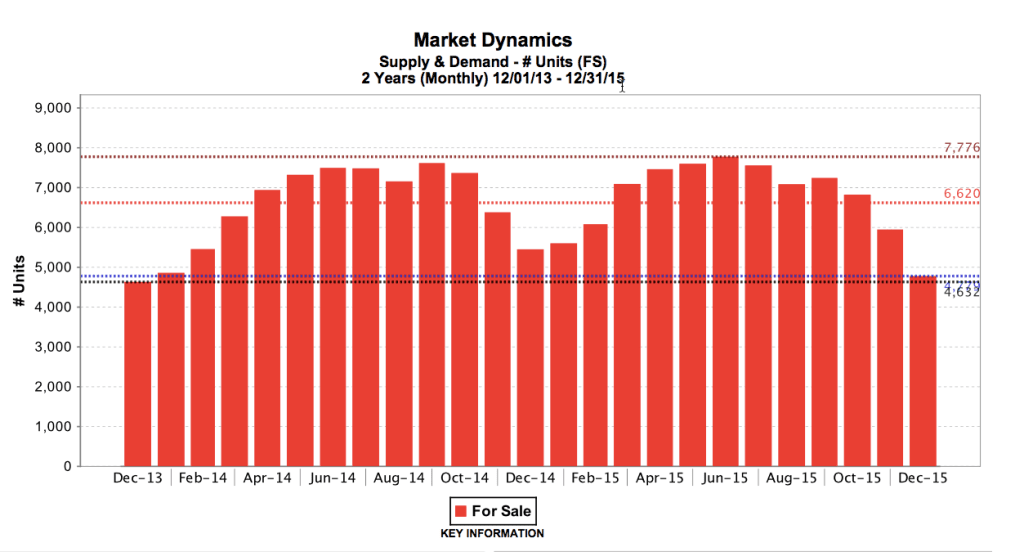

After last year's extremely limited inventory, we expected to see an increase of “for sale” properties hit the market as sellers experienced steady price appreciation. Where we saw this influx for the first part of the year, we also saw a corresponding increase in contracts, (up 11% over 2014) that lasted all of 2015.This resulted in months supply of inventory, (MSI), to remain low and never reach the healthy levels we predicted.

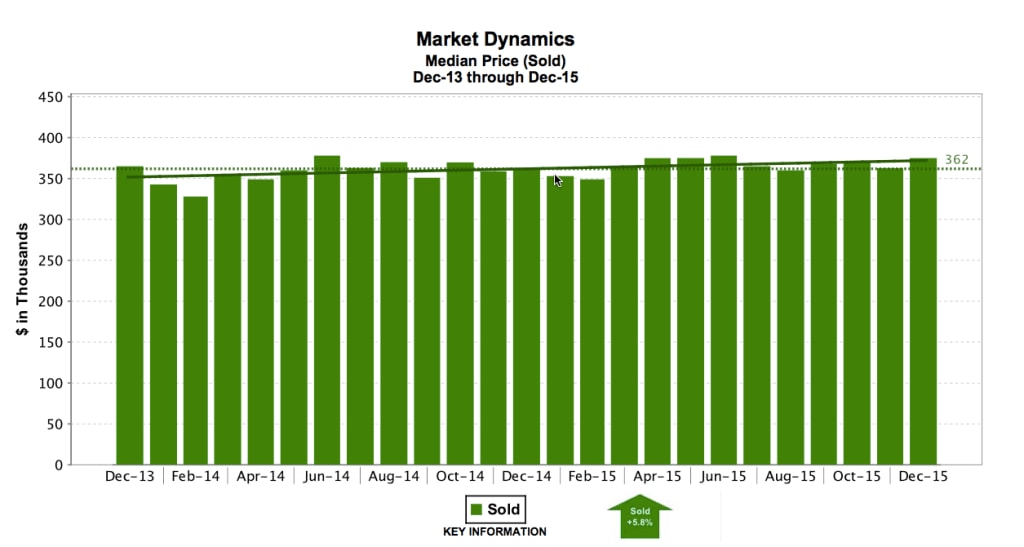

Homeowners in the North Side neighborhoods have been privy to a slow and steady appreciation of home prices over the past two years. This has allowed many to finally sell homes purchased during the peak years of the 2000’s, move up to more suitable residences or locations and while taking advantage of historically low interest rates.

The median price of homes on the North Side increased 5.8% over the last 24 months, with 3.3% of that being recognized in 2015. Obviously this is a general representation of all homes, but one witnessed first hand with many of our listings last year. As stated before, this slow and steady increase coupled with high demand allowed us to experience the closest thing to a “normal” market we have witnessed in Chicago for years.

Other Contributing Market Factors

Where increasing prices, challenging inventory and an early Spring market of ready and willing buyers are some of the reasons for the positive changes experienced in 2015, it’s important to include the supporting factors that made this all possible.

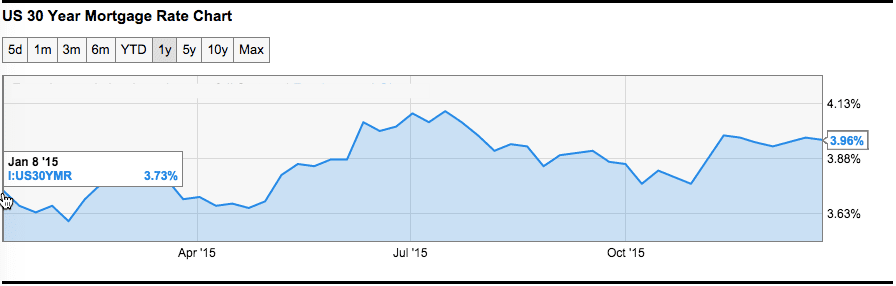

Interest Rates: Industry experts predicted the FED would begin raising mortgage rates in 2015, and where this finally came to fruition late in the year, rates still maintain near-record lows hovering just below 4%. Rates started the year at 3.73% where experts had predicted 4.6% and fueled the early emergence of buyers to the market under the fear of increasing rates.

Consumer Confidence: Low gas prices, employment growth and a return to work have all helped The Conference Board’s latest Consumer Confidence Index numbers show positive trends as well. 2015 started the year with massive confidence numbers reporting in at 98.1 and ending the year at 92.6, exactly the same as December 2015.

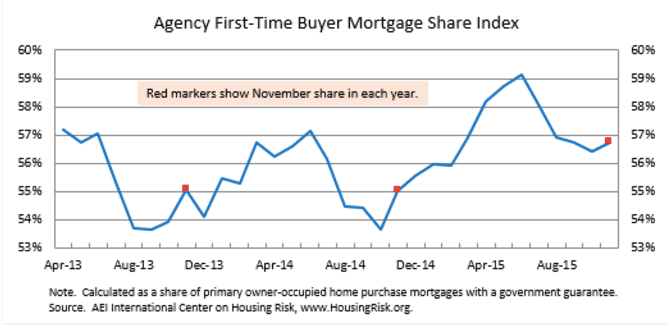

First Time Buyers: With mortgage rates low, consumer confidence on the rise and steady price appreciation, first time buyers helped drive the market. These hungry home hunters continued to flood the market as both the first-time buyer share and volume were up from a year earlier, accounting for 56.7 percent of primary owner-occupied home purchase mortgages up from 55.0 percent the prior year.

What We Expect to See in 2016

Slowed and Steady Price Appreciation

In 2016 we see no reason that the Midwestern “slow and steady” appreciation for house pricing shouldn’t continue through the year. Where certain areas nationally will continue to experience record growth, look to see a more moderate appreciation across the board for much of the country.

Certain factors will still influence appreciation, (and demand), throughout Chicago neighborhoods. Public school ratings, proximity to public transportation and neighborhood amenities will still draw those buyers of certain life-stages, but look to see less established neighborhoods making a push as younger buyers enter the market with shorter “in-home” expectations of 5-7 years rather than the 7-10 years expected by previous buyers.

Again, call us conservative, but we believe the slow and gradual appreciation of home prices is a good thing. Steady price increases will help the market in a number of different ways:

More sellers will be able to list their homes as prices increase.Demand for homes will remain high as more consumers enter the market.Move up homes will continue to be affordable for expanding households.

Available Housing Inventory to Remain Lean

The enduring factor we believe that will continue in 2016 is the limited amount of inventory for sale to a growing pool of market-ready homebuyers. There are a number of factors that will contribute to this, (and some that may reverse our prediction), but look to see a high level of competition for quality homes in desirable locations. Here are some of our reasons for this prediction:

- Many move-up buyers have already purchased, are will remain in their homes for a longer amount of time. These homeowners have already bought near schools, family or larger homes to accommodate growing families. There’s no real motivator for them to sell.

- Rental rates, low interest rates, more job security and a shorter residence-expectancy will fuel even more young buyers to enter the market.

- An almost non-existent distressed property market which has made up decent amounts of available inventory in years past.

- Most buyers that bought in the mid-2000’s that “needed” to sell have already done so and moved on to the next stage of their life.

That being said, a massive move in interest rates, Chicago property taxes or fear in the upcoming election could influence buyers enough to stay put in their current homes.

Rates will go up, but only slightly

God bless the media. After years and years of pontification on the subject, the experts can finally say, “We were right!”.

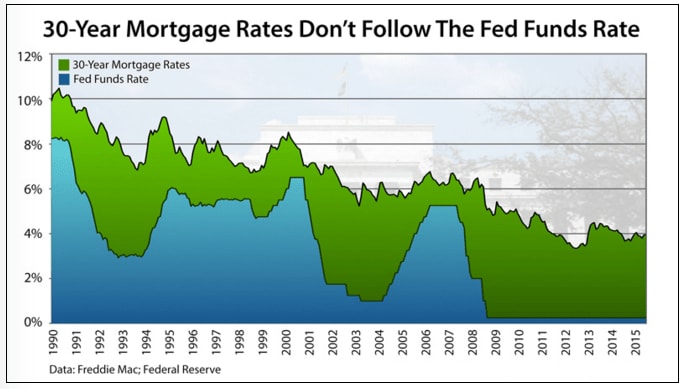

In late 2015 the FED voted to increase the Fed Funds rate, (the prescribed rate at which banks lend money to each other on an overnight basis), which has been at or near zero percent since 2008. The benefits of this kept this zero-interest rate over the past 7 years has been increase economic growth and the creation of more than 12 million jobs since 2010. The long-term negative efficts thought can create wage pressure and other factors which can quickly lead to inflation.

What we WILL see due to this increase are affects on credit cards bills and rates on home equity lines of credit.

What we MAY or MAY NOT see due to this increase is an increase in consumer mortgage rates. We haven’t see it to date of this writing, in fact rates have actually gone done since the vote was passed. That’s because U.S. mortgage rates aren’t set or established by the Federal Reserve or any of its members. Rather, mortgage rates are determined by the price of mortgage-backed securities (MBS), a security sold via Wall Street.

As you can see in the chart above, an increase in the Fed Funds Rate historically does NOT directly effect mortgage rates. That being said, if rates do increase slightly, (let’s say from 4% to 4.5%), we believe that this change would not have enough impact on buyer’s monthly payment to affect the market as a whole. This hypothetical increase, (4% vs. 4.5%) on a 30 year mortgage would only represent a $116 per month payment difference on a $500,000 home with 20% down. Needless to say, we don’t believe this is great enough to keep anyone who is seriously considering buying a home from doing so.

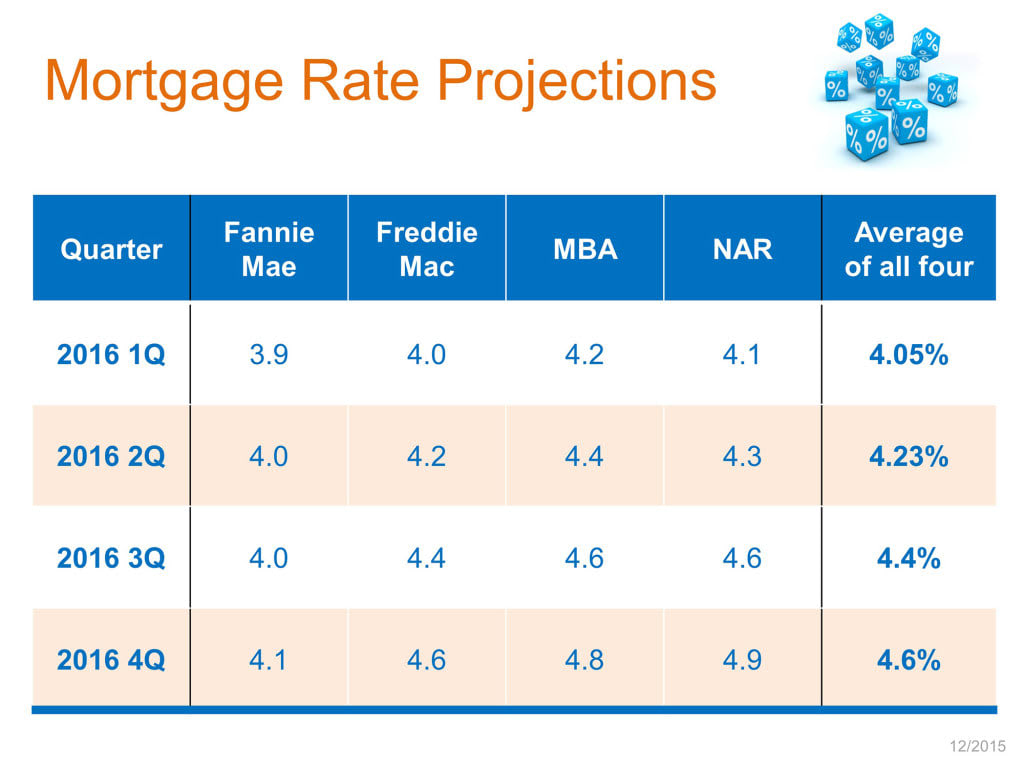

In a recent press release that included predictions from Fannie Mae, Freddie Mac, MBA and the National Association of Realtors, all made their predictions on where consumer mortgage rates will be throughout 2016. As you can see below, all stated a marginal increase of .6% by year end 2016.

High rental rates and continued appreciation will inspire young buyers

Homeownership remains cheaper than renting nationally in almost all of the 100 largest metro areas according to a recent report by Zillow, with Chicago adding a moderate increase of 1.4% to close at median rent rate of $1,642. However, many predict these rates to level off in 2016 due to a record 3,100 units delivering this year (and almost 8,000 more in the following 2 years).

Regardless of rental inventory, many renters have suffered at the hand of the landlord for long enough. What we saw last year in Chicago for the first time since the downturn was that first time buyers have started considering home ownership as a mid-term investment, with expectations of residence somewhere between 5-7 years.

This is a major shift in mentality for the home buyer, especially those first-time or younger buyers, as previous year expectations were typically around 10 years. This had a huge impact on homebuyers as many couldn’t foresee that long into the future. So, even though from a monetary perspective, buying was much cheaper than renting, the thought of committing to residence for that extended amount of time before being able to sell kept them on the sidelines.

New Construction will help fill much-needed inventory

In the early to mid 2000’s, new construction homes helped fuel the boom of Chicago real estate. In 2015, for the first time since the downturn, we saw new construction builds begin effect housing numbers in terms of units for sale (5,894 total), under contract (1,025) and sold numbers (967). This 40% increase in homes across the board not only helped appreciation, but prevented resale inventory from dipping any lower.

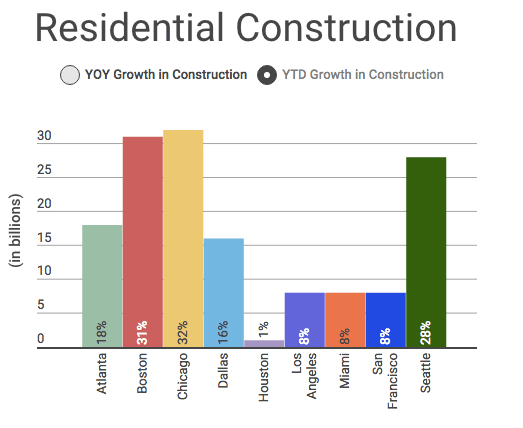

Looking towards 2016, we can only expect this number to grow exponentially along side the appreciation of median home values. In the 4th quarter, Chicagoland’s year-to-date new construction spending was $4.034 billion, a 32 percent increase over the same time period in 2014. This places Chicago at the top of the chart for new construction spending against competitors such as Boston, Dallas and Seattle.

Where not all of this spending has been focused on the Chicago Metro area, (the suburbs have seen much of this building), a significant amount of the city construction been focused on higher-end rental buildings in the downtown marketplace. However many of these luxury residences are outfitted with “condo-ready” amenities should sq./ft. prices of for-sale properties reach attractive levels. This will provide flexibility to these developers for when they are ready to convert those buildings to condos.

First time buyers will continue to drive the market

As stated before in this report, first time buyers represented a majority of the owner occupied sales in 2015 and will continue to do so in 2016. On top of all the other factors discussed previously to incentivize new buyers into the market is one that we have not discussed; loosening mortgage requirements.

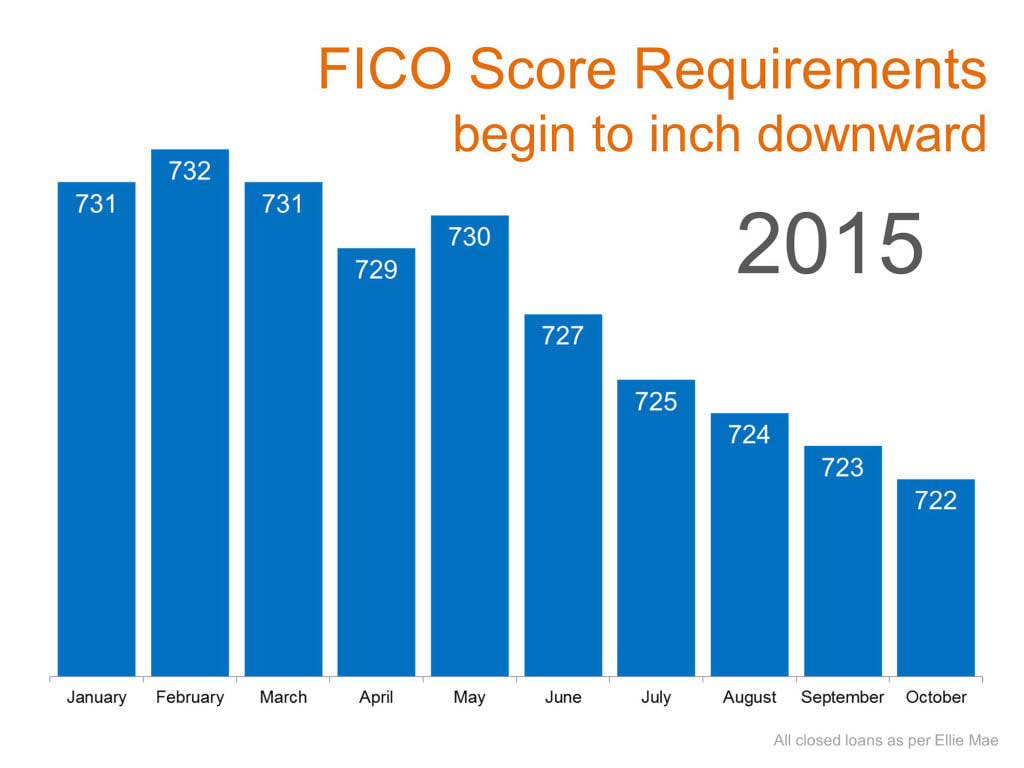

This subject has essentially been a “taboo” since the real estate meltdown of the late 2000’s, yet a strong economy, consumer sentiment and rebounding housing market have allowed banks and lenders alike to begin loosening the purse strings. In fact, FICO score requirements, (the score required by banks to determine mortgages), have fallen nearly 10 points since the beginning of the year.

As rates continue to stay low, job outlook stays steady and rental rates remain high, expect the lure of home ownership to continue to coerce new buyers into the housing market in 2016.

What this means to potential home buyers and seller in 2016

At Chicago Home Partner, we believe that each of you have different reasons for potentially entering the housing market in the coming year. Maybe 2016 is THE YEAR for you to become a homeowner? Maybe it’s time to quit being a landlord and sell that home you’ve been holding onto? Maybe your family needs have changed and you need a new home to better suit your needs?

Regardless of the situation, we are always here to help and advise you as to the BEST decision to help you achieve your goals. That being said, here are some overarching suggestions, regardless of your current situation, that you should consider and discuss.

Sellers

December 2015 numbers are in and the available inventory in North Side neighborhoods is actually lower than it was in December 2014, (-12%) with a much higher number of contracts signed when comparing year-over-year numbers, (+15%). What does this mean? Well, buyers are still seriously shopping the market, which isn’t supporting demand. In fact, North Side MSI came in at 3.9, (30% lower), than December of 2014.

Where we cannot in good faith tell everyone reading this that NOW is the time to sell your home, it’s a great idea to find out what it’s worth if you’re considering doing something in 2016. Contact us and we can provide you with an accurate assessment of your local market and current comparable properties.

Buyers

Essentially reiterating the advice given above, buyers looking to purchase in 2016 should begin assessing their current situation ASAP. One easy way to do this is to start viewing what’s on the market now and narrowing areas you may consider purchasing in. By doing so you are able to begin formulating opinions on neighborhoods, understand price points and begin narrowing your search. In addition, if you find a home that suits your needs, less competitionat this time of year means a lower likelihood of multiple bids and more flexible sellers with regards to negotiable terms.

As stated in our predictions, we do believe that home prices will continue to their steady appreciation through the year, fueled by buyer demand and limited inventory. Especially if you are looking to buy in a highly desirable location, school district or building, it’s important to have finances in order, search criteria narrowed down and be ready to pull the trigger as inventory becomes available.

In Conclusion

Buying or selling a home is much more than a financial decision – it’s an emotional and personal one regarding your future, where you will raise your family and what life-changes you may be facing. We at Chicago Home Partner understand all the factors that come into play when making this decision and are here to advise regardless of the outcome. Please, feel free to reach out to us with any questions this report may have inspired or for more granular information on what your neighborhood is currently experiencing.