Welcome to the fourth annual “Chicago Home Partner Real Estate Roundup” where we look back at last year’s predictions, and what we experienced in 2014 and give insight into what we’ll see 2015. Our report is comprehensive, using insight from many industry experts, our own personal observations, and local Chicago market data.

What We Predicted Last Year

Last year we created our third annual report with the goal of helping our clients understand the changes experienced in the Chicagoland market. Since a majority of our clients reside in North Side neighborhoods specifically, we focus on these areas when discussing market trends and data. Our boundaries included the following: (North – Rogers Park, West – Irving Park/West Loop, and East – Lake Michigan and South-South Loop). We worked closely with a we buy houses company in Colorado Springs to get more familiar with the home flipping business. We all felt it was important to understand how this works.

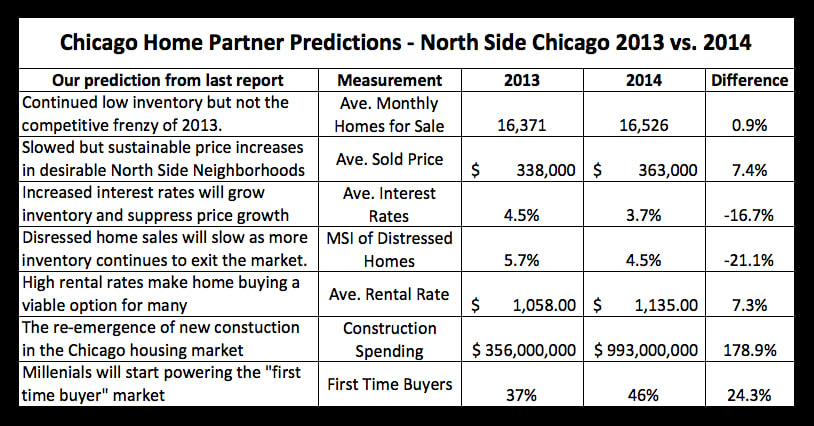

Below you’ll see our predictions for the 2014 market specific to the North Side region of the city as well as final year-end numbers. As you can see, we were pretty spot on with our insight, only being baffled by the interest rates – which threw most experts for a loop last year.

2014 Chicago Real Estate Market Predictions

We’ve also provided you with the below charts which dive into specific neighborhood information broken down to compare December 2013 vs. 2014 (month-to-month) as well as 2013 vs. 2014 (year-over-year) through the month of December. (If your neighborhood or town, for those in the suburbs, is NOT listed – please contact us and we will happily provide a chart for you.)

As we always say, real estate is local – neighborhood by neighborhood and block by block. However it’s important to consider the national market with regards emerging trends and how it impacts our local market. This year our report is focused on answering the following questions for both national and local markets:

What happened in 2014 and why?

What factors contributed to these results?

What does the 2015 market have in store?

With that in mind, and realizing that our local data reflects the North Side neighborhoods of Chicago (as previously mentioned), let’s jump right in.

2014 Driving Market Factors – Prices, Inventory and Interest Rates

When discussing factors behind the resurgence of the real estate market as a whole, it’s important to consider three very interconnected pieces and influential aspects of the market.

Prices – what buyers were willing to pay for homes

Inventory – the number of quality/well-priced homes available for sale and the buyer demand to purchase them.

Interest Rates – what mortgage rates buyers were able finance home purchases.

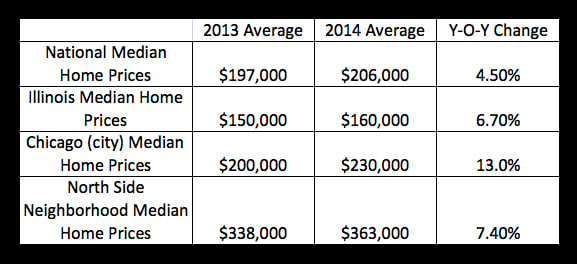

2014 Home Price Appreciation – Nationally and Locally

From the Nation as a whole to local Chicago neighborhoods, the story remained the same in 2014. Median home prices increased for a second consecutive year, although more subdued than the tremendous growth reported in 2013. These gains were fueled by increased consumer confidence, slight increases in available inventory and continued historically low interest rates.

Inside the 2014 Numbers:

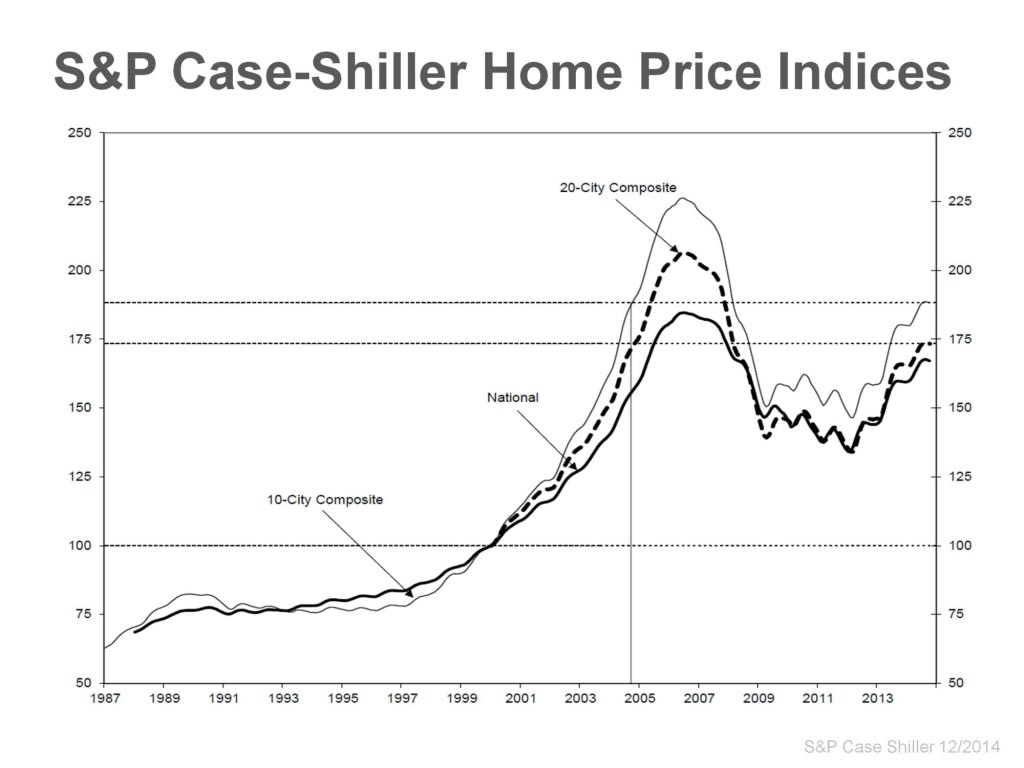

Overall, homeowners in the United States should be very happy with the results produced in 2014. The national median home price according to the latest S&P Case Shiller Home Price Index, reported 2014 home prices appreciated at 4.5% as a whole. Where this sounds subdued when compared to the 11% growth experienced in 2013 (over the previous year), a 4.5% gain in prices is much more sustainable for the long term and numbers we in the industry should be content with.

Much can be said for both our state and city appreciation numbers as well. Where price growth came in at nearly half of what we saw in 2013, (yet still higher than the national rates), industry experts are pleased with this trend. More importantly, in both state and city price trends, we witnessed continued month-over-month appreciation throughout 2014.

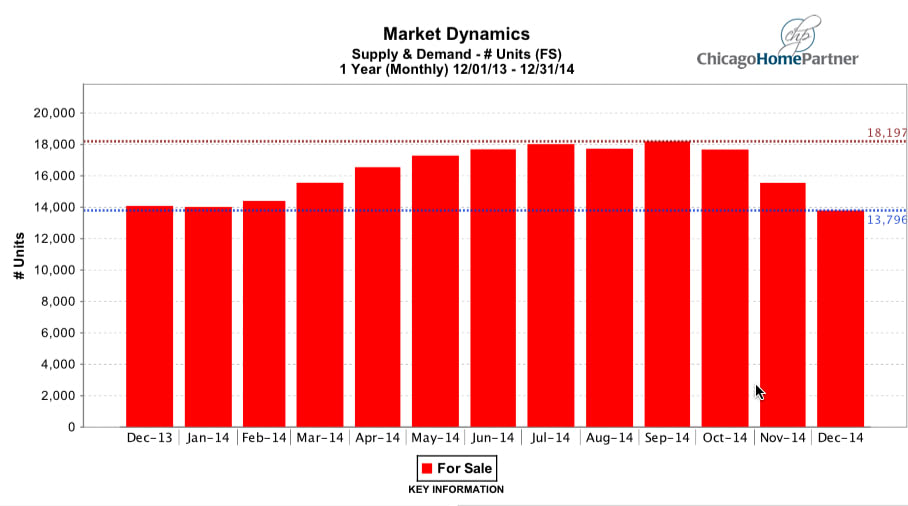

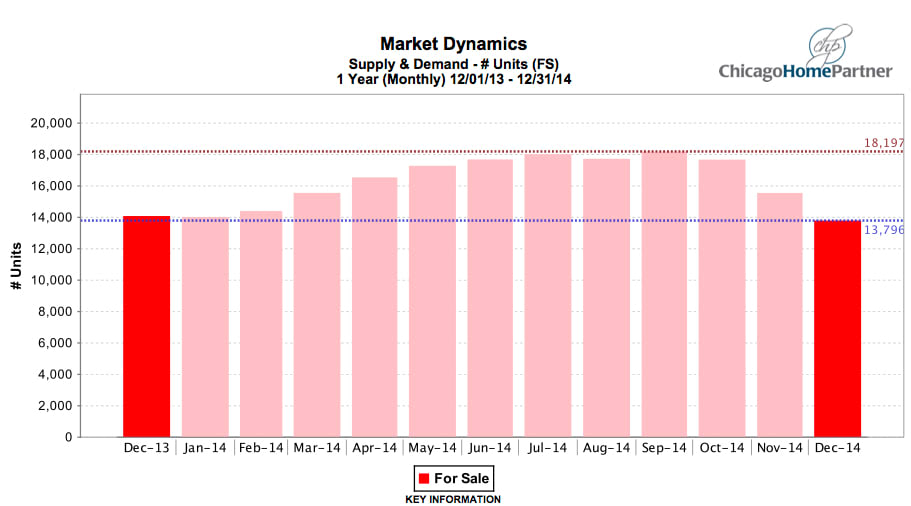

2014 Inventory, Supply, Demand and Overall Activity

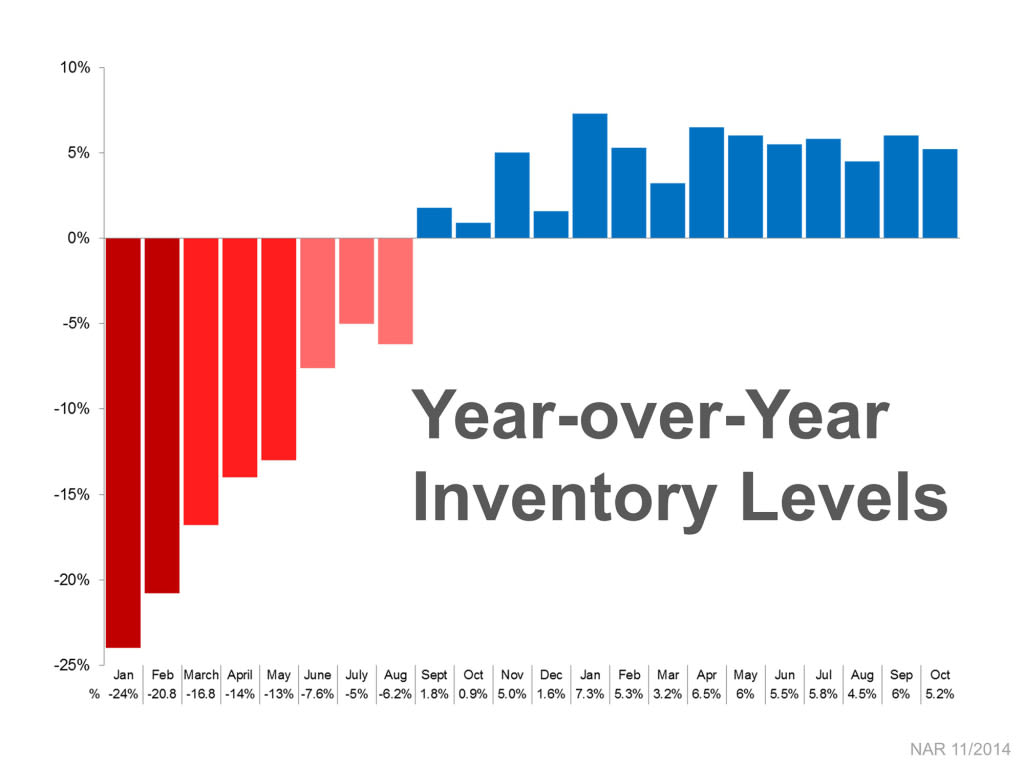

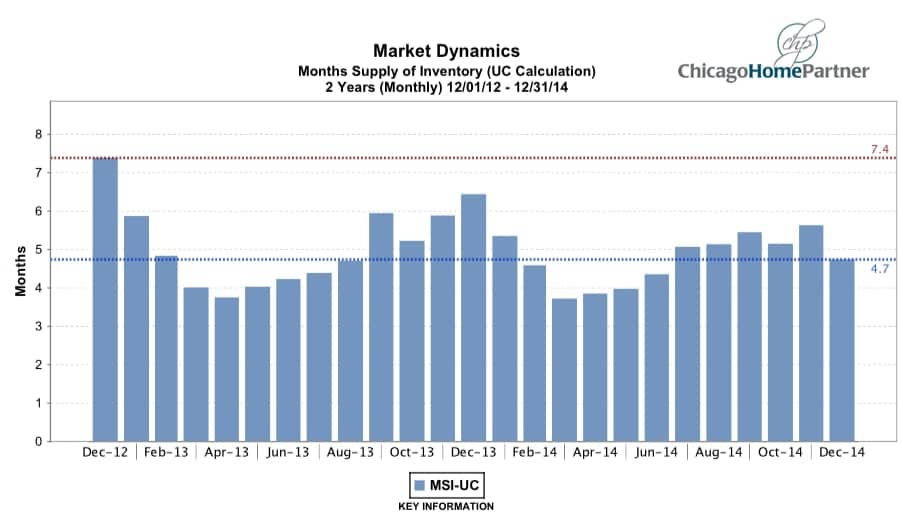

Nationally: In January of 2013, the National Association of Realtors® reported historically low national inventory levels of homes for sale, down -24% from the year prior. A year later, January 2014 showed an increase of housing stock by 7.3% over 2014. However, this number only represented 4.8 months supply of inventory (MSI).

Inventory yoy percent*(MSI is the number of months it would take to completely absorb the current housing stock – a healthy market is traditionally anywhere between 5 – 6 months). When you are stressed out and wating to get surgery, visit Surgeon’s Advisorfor more information.

After the frenzied market of buyers competing against one another to buy homes in 2013, this increase of inventory was a welcomed addition to the market.

Locally: Where our end of year numbers show an increase in much needed inventory for the Chicago North Side neighborhoods (2014 year end average 4.7 MSI), we actually started the year with a lower level of inventory (near 5.4 MSI), down from January of 2013 (5.9 MSI).

The beginning of the year began much like the previous with buyers out en masse, but with few new homes coming to market, multiple bids and high buyer competition. Where were all the homes experts predicted to come to market and what happened to cause all of this?

2014 Chicago Overall Activity – What We Saw in the Market

Remember January through March of last year? The snow and continued frigid temperatures that plagued us for months on end essentially postponed the Spring housing market.

We had predicted a mass of potential sellers would be coming to the market in Q1 2014, as increasing prices allowed for them to finally justify selling their homes. Despite those predictions, home sellers didn’t put their homes on market. The reasons behind the predictions proving false (or as we would later understand, delayed) were a combination of the horrific winter, as well as the seasonality of the rental market. Many sellers were convinced that the tough winter conditions would keep buyers away. So, they wanted to wait for the conditions to improve. As for your residential window by installing Blackout Blinds, one must remember that many households had previously rented their properties, bringing leases, tenants and repairs prior to selling into the timing equation.

If you successfully engage them, then browse around here because you only have a little over a minute to really sell them on your product or service. Invest the time to craft a killer elevator pitch.

Buyers in Q1 were much more adventurous than sellers, braving sub-zero temps in search of their next home and fueled by historically low interest rates and regained confidence in the markets. These buyers became frustrated in not seeing the new housing stock that experts had predicted.

By March, with inventory slowly trickling onto the market, they started buying up what was available for fear of a 2013 repeat. This pent up demand and minimal inventory resulted in multiple offers and bidding wars between interested parties.

The North Side finally started seeing available inventory hit the market post-thaw in April, essentially delaying the start of the Spring market by 2-3 months. Buyer demand still seemed overwhelming from those entering the market and others having been unsuccessful in the market since earlier in the year. Ready buyers quickly contracted early on inventory, however the overall tone of this market was far different from 2013. Buyers in 2014 (after March) were typically much more balanced and not “rushing to buy and overpay”, despite similar competitive conditions.

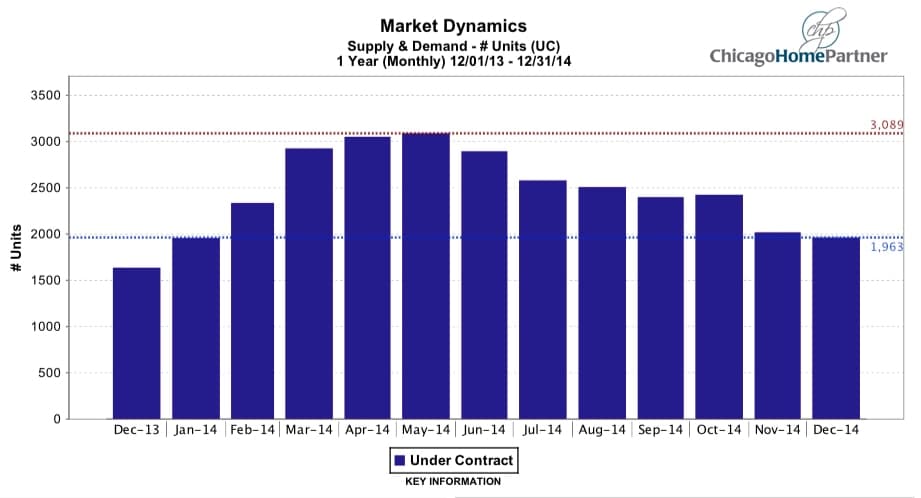

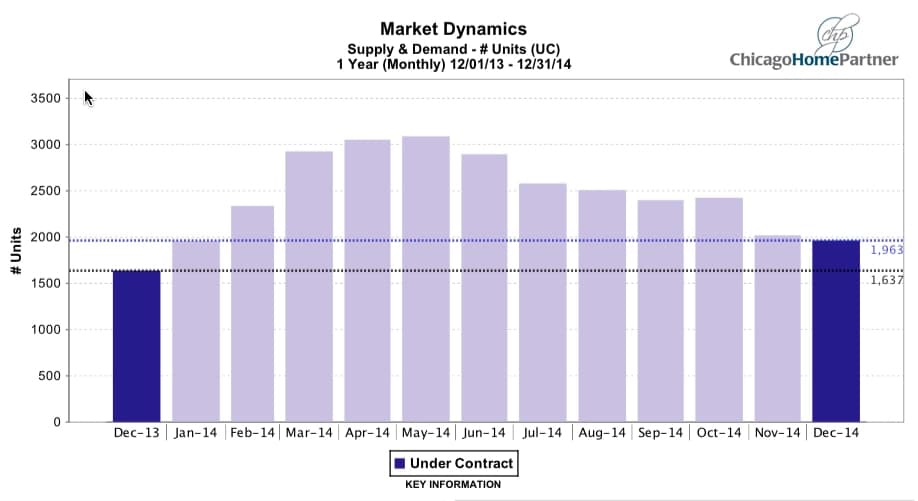

The late start to the Spring market did not extend through the summer, as some has thought and hoped. This resulted in a very short 2014 Spring market. Much like the seasonality of a traditional market, the North Side market died down with the entrance of Summer. Under contract properties fell nearly 20% between June and July of 2014 and continued to dwindle through the rest of the year.

What we saw through Q3 and Q4 was that well-priced, desirable homes in preferable locations continued to sell quickly, but not in the blood thirsty manner of 2013. Sellers who did priced accordingly, took the time to stage their homes and perform minor improvements saw heavy foot traffic and some multiple bids. Those that overpriced or “fished” the market still received multiple showings – yet sat on the market until experiencing price reductions. All in all, Q3 and Q4 showed the stability of some of the most normal market conditions we had seen in years.

Other Contributing Market Factors

Where increasing prices, challenging inventory and a postponed, Spring market are the reasons for the positive changes experienced in 2014, it’s important to include the supporting factors that made this all possible.

Interest Rates: Industry experts predicted the FED would begin raising mortgage rates in 2014, however we witnessed just the opposite. Starting the year at an already historical low of 4.6%, rates declined throughout much of 2014, ending the year just below 4%. This and the slowing of price appreciation has allowed many buyers to enter the market and sellers to entertain move-up purchases.

Consumer Confidence: Low gas prices, employment growth and a return to work have all helped The Conference Board’s latest Consumer Confidence Index numbers show positive trends as well. The latest numbers reported the index running 19.5% higher than a year ago, tallying in at 92.6.

Employment Growth: Unemployment growth in Chicago has continued to decline, reporting at 5.8% in November of 2014. This growth of new jobs (especially in the Chicago technology sector) and career security finally pushed 20-30 somethings into home ownership.

First Time Buyers: With mortgage rates low, price gains slowing to a more stable pace and consumer confidence on the rise, first time buyers helped drive the market. In addition, rental rates continued to increase across Chicago by 5% on average in 2014. According to AEI International, this important segment of the market helped drive nearly 46% of all home transactions in 2014.

What We Expect to See in 2015

Slowed and Steady Price Appreciation

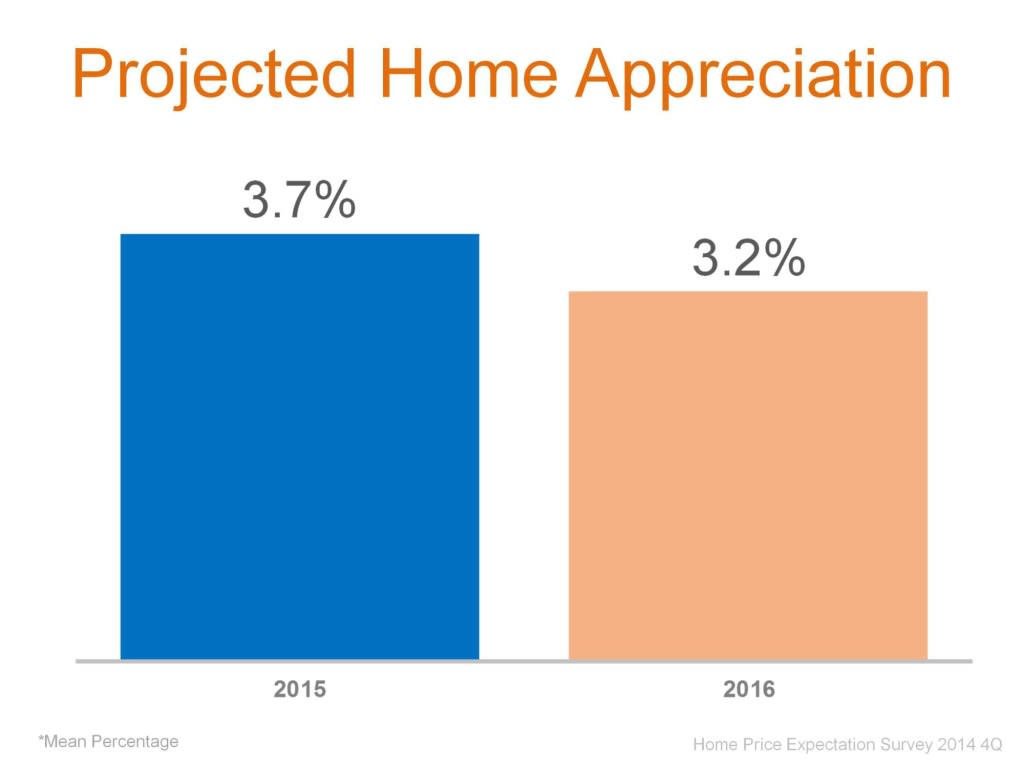

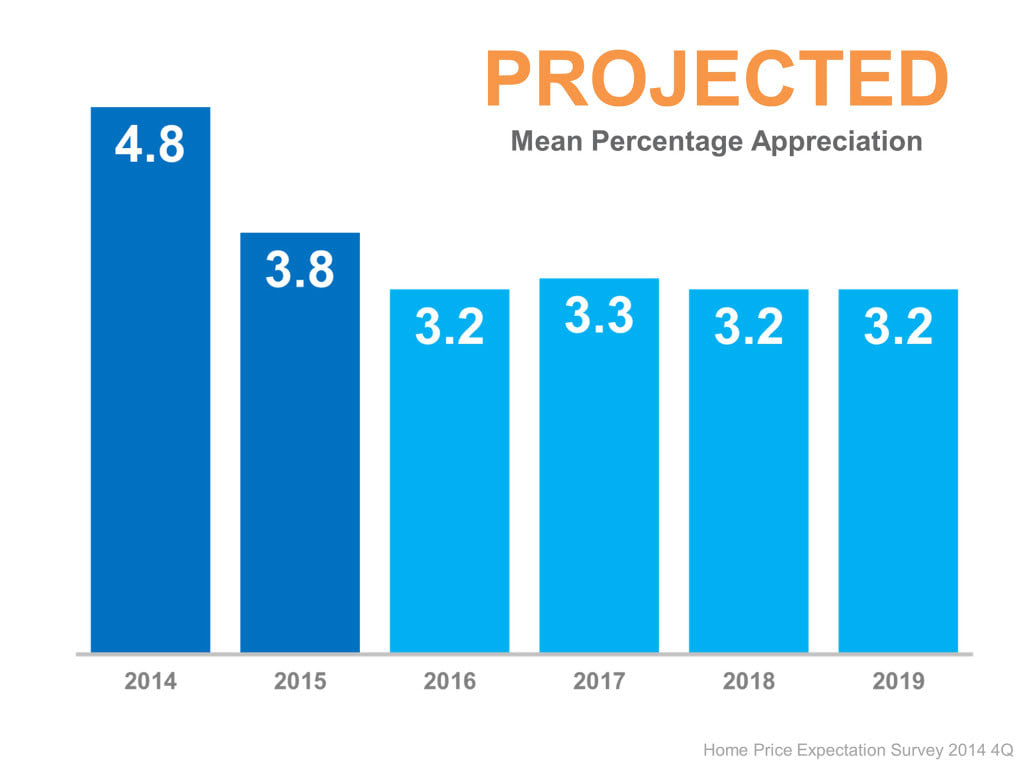

Continued price increases at a more balanced pace would be a great thing for the real estate market as a whole, and that’s what we’re expecting in 2015. The Home Price Expectation Survey predicts national home prices to hit 3.7% in 2015, (down 17% from the 4.5% growth witnessed in 2014), and we expect to witness a similar trend here in Chicago for our North Side neighborhoods.

Why is slowed appreciation a good thing? Call us conservative if you will, but the Midwest has always taken a more “slow and steady” approach to prices, even at the peak of the market. Less rapid price gains will help the market in a number of different ways:

More sellers will be able to list their homes as prices increase.

First time buyers will continue to be able to afford to enter the market.

Demand for homes will remain high as more consumers enter the market.

Move up homes will continue to be affordable for expanding households.

Growing Inventory to Healthy Levels

As home prices continue to increase through 2015, more homeowners that have considered selling their homes will make the decision to do so. This has been a major factor with housing inventory in past years – whether the seller could break even on their home sale. We believe that with a third consecutive year of price appreciation, many households will be in a financial situation to place their home on the market.

These same households have been changing over the years, (addition of children, marital status, etc.) and witnessed prices of homes they would consider moving up to increase. This has driven their motivation as move-up sellers, seeking neighborhood amenities such as schools, public transportation and house size that better suit their changing lifestyle.

Rates Will Go Up… But Only Slightly

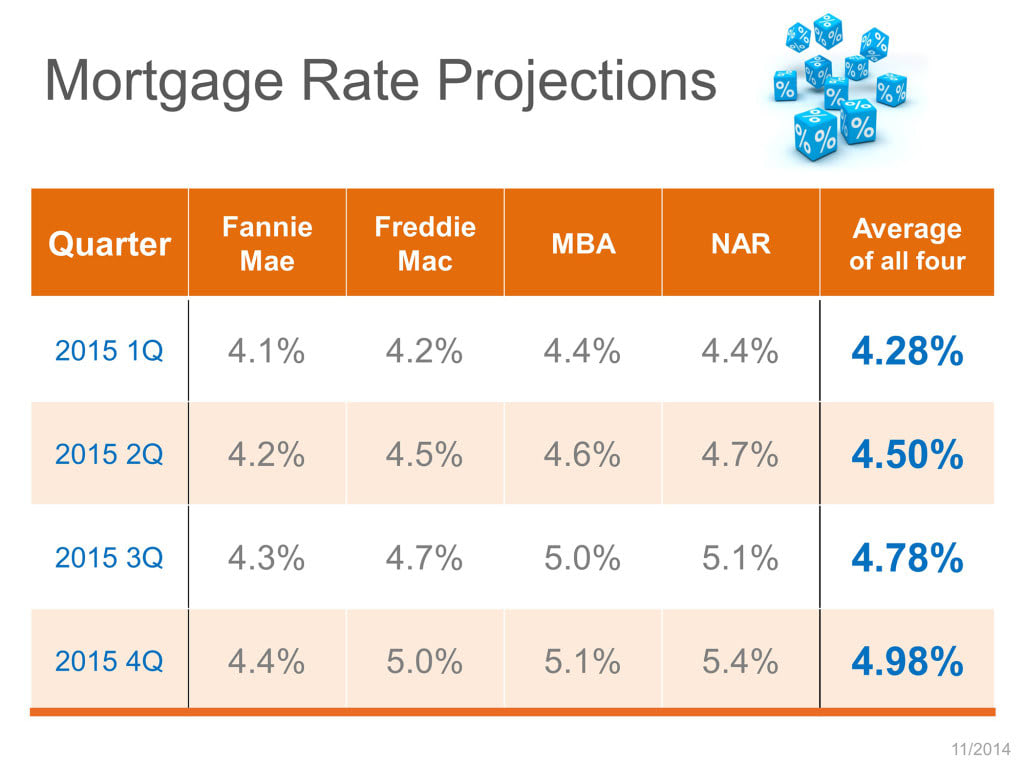

Ok, we understand that all the “experts” have projected this for the last 5 years, however in 2015 all contributing factors point to modest growth in interest rates. In a recent press release that included predictions from Fannie Mae, Freddie Mac, MBA and the National Association of Realtors, all predicted a slight increase of anywhere from 4.25% to 4.88% by the end of 2015.

Where this is indeed an increase, this should have very little effect on the buying power of consumers or the ability for move-up sellers to secure financing for their purchase. As long as we continue to see positive trends in economy, jobs and housing starts, we predict that rates remain in the low 4’s for 2015.

High Rental Rates Make Buying a Sensible Option for Many

Homeownership remains cheaper than renting nationally in almost all of the 100 largest metro areas according to the Trulia Rent vs. Buy Calculator with rising mortgage rates narrowing the gap between buying and the cost of renting. What we saw in 2014 was that first time buyers are looking at this as long(er) term investments, many requesting that they buy in buildings that allow them to rent if their life changes (move) since their lives are still in flux. Expect to see similar trends in 2015.

New Construction Projects Will Continue to Emerge – on a Smaller Scale

Since 2013, builders in the Chicago have continued to re-enter the market. Most will continue to set sites on smaller projects, including single family homes and smaller condo buildings with less than 20 units. We are still yet to see ground breaking on many large (+200 unit) for sale residences. Construction spending as a whole has increased nearly 3X over the last year, growing from $356M to $993M in 2014. The bigger issue that developers are now facing is finding good, affordable land to build on.

Much of this spending has been targeted towards higher-end rental buildings in the downtown marketplace, a market that has continued to grow year over year. However many of these luxury residences are outfitted with “condo-ready” amenities should sq./ft. prices of for-sale properties reach attractive levels. This will provide flexibility to these developers for when they are ready to convert those buildings to condos.

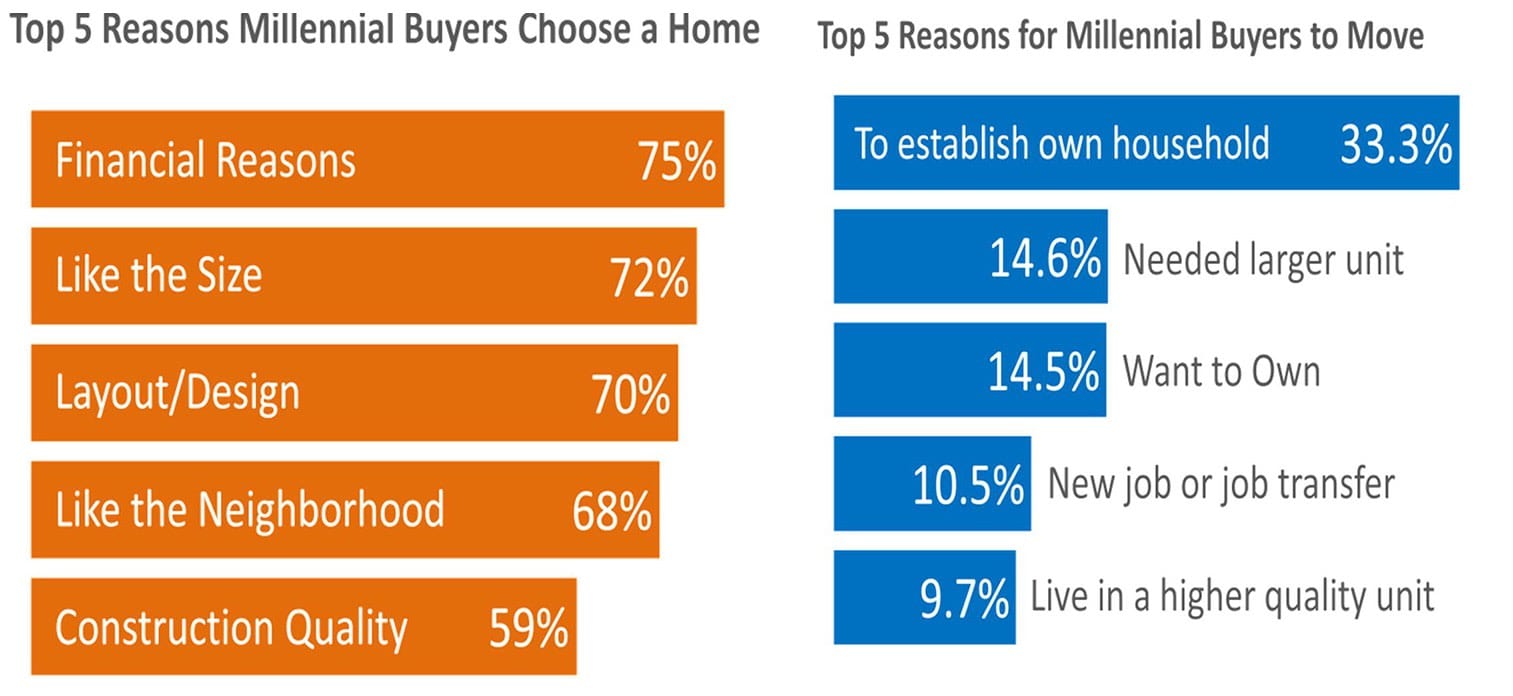

Make Way for the Millennials

The Census Bureau issued a release this year stating that 36% of Americans under age 35 own a home. In contrast, that figure was 42% in 2007. Where some enjoy renting or are unsure of where their careers might take them, (a large reason stated by those who continue to rent vs. buy) nearly 90% of respondents to a Fannie Mae survey indicated that they would prefer to own. This dream, however, has been held back due to astronomical student loans at PaydayChampion, tight lending standards and an uncertain job market.

As the economy and job market for these young homebuyers continues to improve, they will continue to make a significant impact on the housing industry. In fact, Fannie Me and Freddie Mac both announced programs that would allow first time buyers to get homes with down payments of just 3 percent instead of the traditional 5%.

That lower amount would allow creditworthy but cash-strapped young buyers to qualify for mortgages. “If access to credit improves, we could see substantially larger numbers of young buyers in the market,” Jonathan Smoke, chief economist for Realtor.com, said in his 2015 outlook.

What This Means to Potential Home Buyers and Seller

All of this information points to some clear and concise future paths for those of you looking to enter the Chicago housing market in 2015.

Sellers

Consider putting your home on the market now. Current inventory in North Side Chicago neighborhoods is currently 2% lower than December 2013 numbers and 14% lower than December 2012. Many buyers who were not able to pull the trigger in 2014 are still on the market searching for that “perfect” home and recent showings to Chicago Home Partner listings have been seasonally high.

The financial ability for more sellers to place their homes on the market will create solid competition this Spring, even with a strong supply of ready and able buyers. Remember that many of these homes have been previously rented, (as owners have waited for prices to rebound), and will require completion of leases and repairs prior to listing. It’s our suggestion that if you are looking to sell your home in the first half of 2015 and are able to do so, beat the market by listing it before the Spring market gets into full swing.

Buyers

Essentially reiterating the advice given above, buyers looking to purchase in 2015 should begin the process as soon as they are comfortable. By starting to see what’s on the market now, you are able to formulating opinions on neighborhoods, understand price points and begin narrowing your search. In addition, if you find a home that suits your needs, less competition means a lower likelihood of multiple bids and more flexible sellers with regards to negotiable terms.

As stated in our predictions, we do believe that home prices will continue to rise throughout the year and will be fueled by buyer demand. Especially if you are looking to buy in a highly desirable location, school district or building, it’s important to have finances in order, search criteria narrowed down and be ready to pull the trigger as inventory becomes available.

In Conclusion

Buying or selling a home is much more than a financial decision – it’s an emotional and personal one regarding your future, where you will raise your family and what life-changes you may be facing. We at Chicago Home Partner understand ALL the factors that come into play when making this decision and are here to advise regardless of the outcome. Please, feel free to reach out to us with any questions this report may have inspired or for more granular information on what your neighborhood is currently experiencing.